When it comes time to sell your Alabama property, the path you choose can dramatically impact how much money actually ends up in your pocket. While most homeowners automatically assume a traditional MLS listing is the only option, savvy sellers are discovering that seller financing can often deliver superior net proceeds—sometimes by tens of thousands of dollars.

Let’s break down the real numbers behind both approaches so you can make an informed decision that maximizes your financial outcome.

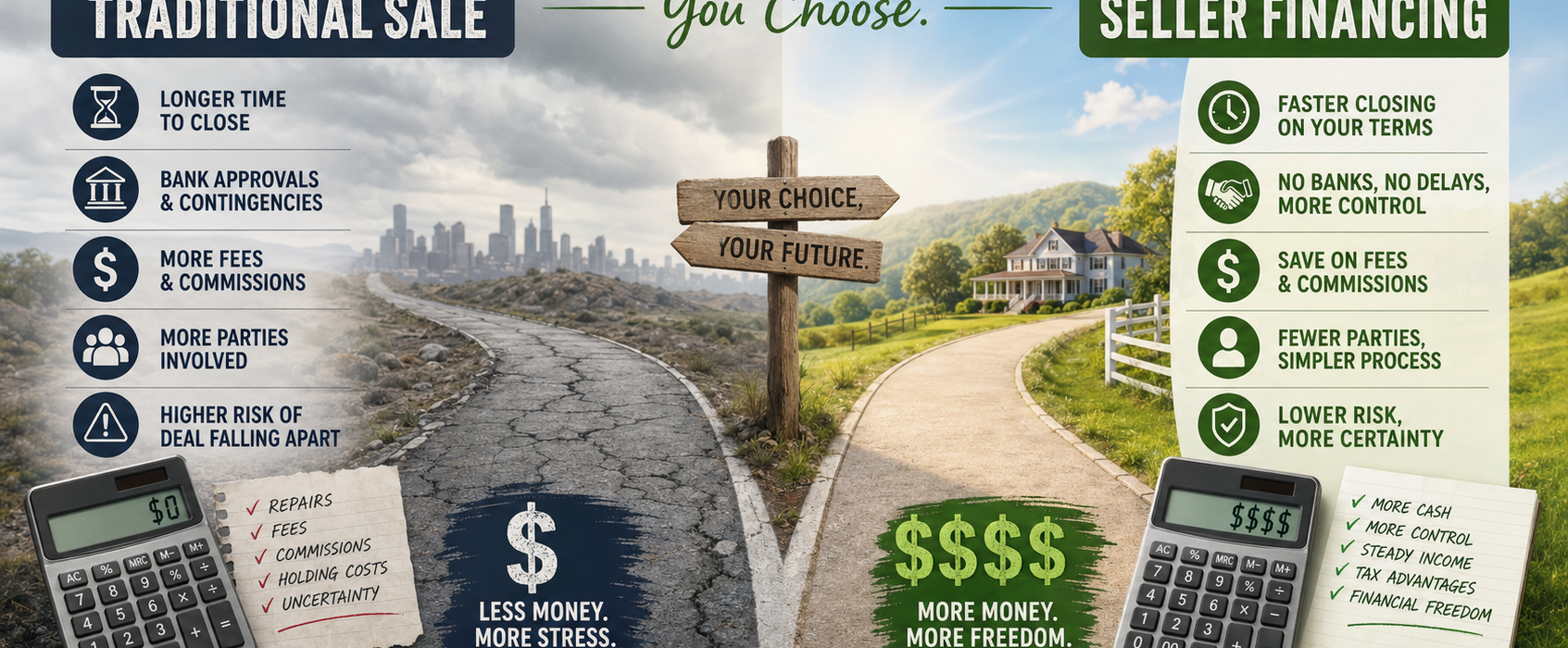

The Hidden Costs of Traditional Sales

Traditional real estate sales come with a hefty price tag that many sellers don’t fully appreciate until closing day. According to 2026 industry data from Clever Real Estate, the average real estate commission has risen to 5.70%, up from 5.44% in 2025. On top of that, sellers typically pay an additional 1-3% in closing costs.

Real Numbers: What a $300,000 Traditional Sale Actually Costs

Let’s examine a typical Alabama home sale:

Sale Price: $300,000

Traditional Sale Costs:

- Real estate commissions (5.70%): $17,100

- Closing costs (2% average): $6,000

- Repairs/staging (conservative estimate): $5,000

- Holding costs during listing period: $2,000

Total Costs: $30,100

Net Proceeds: $269,900

That’s over $30,000 in costs before you see a dime—and this assumes your home sells relatively quickly without major price reductions.

The Seller Financing Advantage: A Different Financial Picture

Now let’s look at the same $300,000 property sold using seller financing, also known as owner financing. This is where you act as the bank, allowing the buyer to make monthly payments directly to you over time.

Real Numbers: The Same $300,000 Home with Seller Financing

Sale Price: $300,000 (often higher with seller financing)

Seller Financing Costs:

- Real estate commissions: $0 (direct sale)

- Closing costs: $1,500-$2,000

- Repairs: $0 (sold as-is)

- Staging: $0

Immediate Costs: $2,000

Down Payment Received (typical 10-20%): $10,000-$60,000

But here’s where it gets interesting—the long-term financial benefits.

The Cash Flow Goldmine

With seller financing, you’re not just selling a house—you’re creating an income stream. Let’s say you structure the deal with:

- Sale Price: $300,000

- Down Payment: $40,000 (13%)

- Financed Amount: $260,000

- Interest Rate: 10% (typical for seller financing)

- Term: 30 years

Your monthly payment: $2,281

Total interest earned over 30 years: $561,160

Yes, you read that correctly. Instead of walking away with $269,900 after a traditional sale, you could ultimately receive $861,160 ($300,000 principal + $561,160 interest) over the life of the loan.

Even if the buyer refinances or pays off early (which often happens within 5-7 years), you’ll still earn substantial interest income while enjoying monthly cash flow.

The Tax Advantage: Installment Sale Treatment

Here’s another critical factor most sellers overlook: capital gains taxes.

Traditional Sale Tax Hit

When you sell traditionally, you pay capital gains tax on your entire profit in the year of sale. If you’ve owned your home for years and have significant appreciation, this can mean a substantial tax bill.

Example:

- Purchase price (10 years ago): $150,000

- Sale price: $300,000

- Capital gain: $150,000

- Federal capital gains tax (15% for most sellers): $22,500

- State taxes may apply

Seller Financing Tax Benefit

With seller financing, you can use installment sale treatment, spreading your capital gains tax liability over the years you receive payments. This means:

- Lower annual taxable income

- Potentially staying in a lower tax bracket

- More control over when you recognize gains

- Significant tax savings over time

According to IRS guidelines, you only pay capital gains tax on the portion of principal you receive each year, not the entire gain upfront. This can save Alabama sellers thousands in taxes annually.

When Does Each Strategy Make Sense?

Choose Traditional Sale When:

✅ You need 100% of your equity immediately

✅ Your home is in pristine, market-ready condition

✅ You’re in a hot seller’s market with multiple offers expected

✅ You don’t want any ongoing involvement with the property

✅ You have time to wait for the right buyer (average 30-60 days in Alabama)

Choose Seller Financing When:

✅ You want to maximize total proceeds over time

✅ You’re looking for steady monthly income

✅ You want to minimize upfront costs and taxes

✅ Your property needs repairs you’d rather not make

✅ You’re open to creative deal structures

✅ You want to sell faster (seller financing attracts more buyers)

✅ You’re comfortable with the buyer making payments over time

The Alabama Market Reality in 2026

The Alabama real estate market has shifted significantly. With inventory up 28.9% year-over-year as of late 2025, we’re moving from a seller’s market to a more balanced market. This means:

- Homes are taking longer to sell

- Buyers have more negotiating power

- Traditional sales may require price reductions

- Creative financing options become more attractive

In this environment, seller financing can be your competitive advantage—attracting buyers who can’t qualify for traditional mortgages while commanding a premium price.

Real-World Scenario: Side-by-Side Comparison

Let’s put it all together with a realistic Alabama property:

Property Details

- 3-bedroom home in Birmingham suburbs

- Current market value: $250,000

- Owned for 8 years, original purchase: $180,000

- Needs $8,000 in repairs for traditional sale

Option 1: Traditional MLS Sale

- List price: $250,000

- Repairs/staging: -$8,000

- Commission (5.70%): -$14,250

- Closing costs: -$2,000

- Net proceeds: $225,750

- Capital gains tax (on $70,000 gain): -$10,500

- Final net: $215,250

Option 2: Seller Financing

- Sale price: $260,000 (5% premium for terms)

- Down payment (15%): +$39,000 (immediate)

- Financed: $221,000 at 10% for 20 years

- Monthly payment: $2,132

- Closing costs: -$2,000

- Immediate cash: $37,000

- Monthly income: $2,132

- Total over 20 years: $551,680

- Tax benefits: Spread over 20 years

The difference? Over $300,000 more in total proceeds, plus significant tax advantages.

Important Note: All the profit calculations above assume you own your property free and clear. In reality, most sellers still have an outstanding mortgage balance that must be paid off at closing.

Your actual net proceeds from either selling strategy will be determined by:

Net Proceeds = Sale Price – Selling Costs – Remaining Mortgage Balance

Common Concerns About Seller Financing (Addressed)

“What if the buyer stops paying?”

You retain the deed until the loan is paid off. If they default, you can foreclose and keep all payments made plus the property. You’re in a stronger position than a traditional lender.

“Isn’t this risky?”

With proper vetting (credit check, employment verification, adequate down payment), seller financing can be very secure. Many sellers require 10-20% down, ensuring the buyer has skin in the game.

“How do I know if a buyer is qualified?”

Work with experienced professionals like Property Prodigy who can help structure deals, vet buyers, and ensure proper documentation. We handle the details so you don’t have to.

“Can I sell the note if I need cash later?”

Yes! Seller-financed notes can be sold to investors if you need a lump sum later. You have flexibility traditional sales don’t offer.

The Property Prodigy Approach

At Property Prodigy, we specialize in helping Alabama homeowners explore all their options—not just the traditional route. We understand that every seller’s situation is unique, and we’re committed to finding the strategy that puts the most money in your pocket.

Whether you’re dealing with:

- A property that needs repairs

- Time constraints

- Tax considerations

- The desire for ongoing income

- A challenging market

We can structure a solution that works for your specific goals.

Want to learn more about how seller financing works? Check out our comprehensive Seller Financing Guide for deeper insights into this powerful strategy.

Making Your Decision: Key Questions to Ask

Before choosing your selling strategy, consider:

- What’s my timeline? Need cash now or can you wait for higher total returns?

- What’s my tax situation? Will spreading gains over time benefit you?

- What’s my property condition? Repairs needed or move-in ready?

- What are my financial goals? Lump sum or steady income stream?

- What’s my risk tolerance? Comfortable with buyer payments or want clean break?

The Bottom Line: Do the Math for Your Situation

While traditional sales offer immediate liquidity, seller financing often delivers:

- Higher total proceeds (often 2-3x more over the loan term)

- Significant tax advantages through installment sale treatment

- Monthly cash flow that can supplement retirement or other income

- Lower upfront costs (save $15,000-$30,000 in commissions and fees)

- Faster sales in competitive markets

- Flexibility to structure deals that work for both parties

The key is running the numbers for your specific property and financial situation.

Ready to Maximize Your Net Proceeds?

Don’t leave tens of thousands of dollars on the table by defaulting to a traditional sale without exploring your options. The difference between seller financing and a traditional sale could mean an extra $200,000-$400,000 in your pocket over time—money that could fund your retirement, pay for your children’s education, or provide financial security.

Ready to explore which selling strategy puts the most money in your pocket? Get your free property analysis from Property Prodigy today.

Contact us at (205) 548-6157 or email info@propertyprdgy.com to schedule your no-obligation consultation. We’ll analyze your specific situation, run the numbers, and show you exactly what each option means for your bottom line.

Your property is likely your largest asset—make sure you’re maximizing every dollar when you sell.

Property Prodigy specializes in creative real estate solutions throughout Alabama, helping homeowners navigate seller financing, cash sales, and hybrid strategies that maximize net proceeds. Whether you’re in Birmingham, Huntsville, Mobile, or anywhere in between, we’re here to help you make the most profitable decision for your situation.